Even as the US government moves cautiously to regulate and adopt cryptocurrency, new surveys show that the use of traditional financial services, such as bank accounts and cash, is already on the decline, especially among young people. clients.

A survey released last week by global payment platform provider Thunes shed light on the shopping, social media and money management habits of so-called “Zoomers” – the Genz generation born between the middle and the late 1990s.

The survey of people aged 16 to 24 living in 13 developed and emerging countries found that Gen Z are embracing new types of money management tools and have relatively little enthusiasm for traditional options like than bank accounts. (In fact, 62% of respondents said they don’t have one.) Mobile wallet usage, on the other hand, is growing rapidly; in some markets, almost half of Zoomers now have a mobile wallet.

The Thunes survey revealed that mobile wallets or virtual wallets are gaining ground: in five of the 13 countries surveyed, mobile wallets were the most popular means of payment. (Mobile wallets store information of a credit card, debit card, coupons and loyalty cards on a mobile device; they are also an essential storage component of cryptocurrency and stablecoins .)

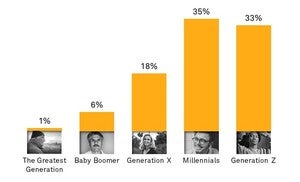

And in a separate 451 Research survey published on March 31, 20% of respondents said they had bought, traded or received cryptocurrencies. The strongest adoption was among Gen Z/Zoomers (33%) and Millennials (35%), ending in single digits for Baby Boomers and the largest generation.

S&P Global Market Intelligence 451 Research

S&P Global Market Intelligence 451 ResearchHave you ever bought, exchanged or received cryptocurrencies (e.g. Bitcoin, Dogecoin)?

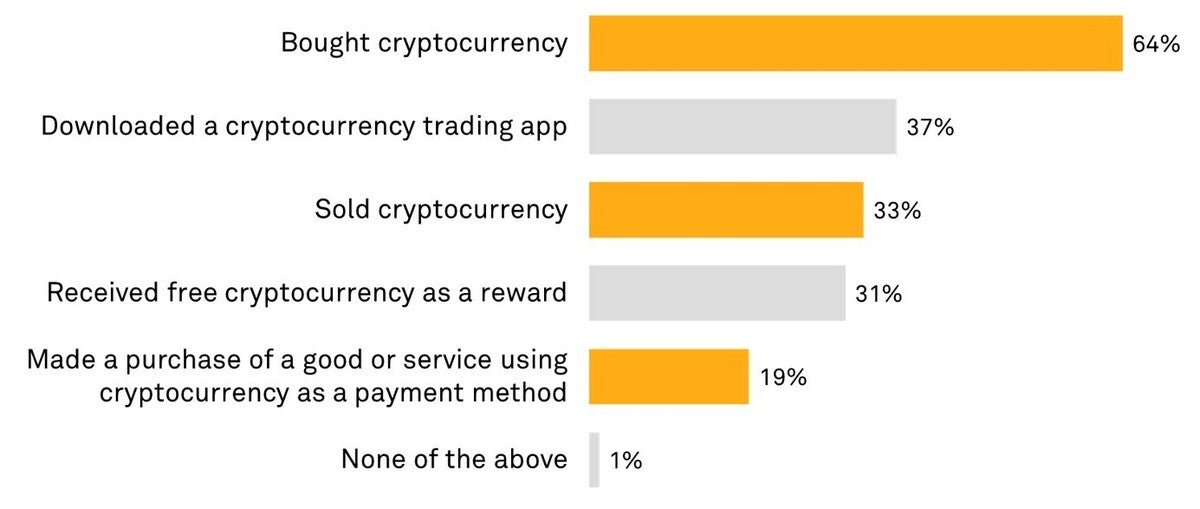

The 451 Research report indicates that more users bought cryptocurrency as an investment tool than used it as a payment method.

“When exploring the specific activities that cryptocurrency participants have engaged in, the message is clear: while most have bought cryptocurrencies (64%), a much smaller percentage are selling them ( 33%), and an even smaller percentage use cryptocurrency as a form of payment (19%),” the report states. “Essentially, most consumers who engage with cryptocurrency treat it like a active, much like they would for a security (e.g. stock).”

On Friday, US Treasury Secretary Janet Yellen weighed in on the idea of a digital dollar, saying it “could become a form of trust currency comparable to physical cash, but potentially offering some of the anticipated benefits digital assets”.

“Digital assets may be relatively new, but they are part of a larger trend – the digitalization of finance – that has been in the works for decades,” Yellen said at an event at American University. “In 1990, there were less than three million Internet users. Today there are about 4.5 billion, and we take it for granted that many aspects of our financial lives can be managed from small internet-connected devices that fit in the palm of our hands.

Yellen also warned that the rise of stablecoins, a form of electronic money tied to government-backed liquidity, raises policy concerns, including those related to illicit financing, user protection and systemic risk.

“And, they are currently subject to inconsistent and fragmented oversight,” Yellen said, adding that the Treasury has worked with the President’s Financial Markets Task Force, the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller. currency (OCC) to study stablecoins.

S&P Global Market Intelligence 451 Research

S&P Global Market Intelligence 451 ResearchRegarding cryptocurrencies, which of the following actions have you taken?

To peg their dollar stablecoin, most issuers back their coins with safe and liquid traditional assets, Yellen pointed out. This way, when a user wants to exchange stablecoins for a dollar, the company has the money to make the exchange.

“But, at the moment, no one can assure you that this will happen. In times of stress, this uncertainty could lead to a race,” she said. “It’s not hypothetical.”

Yellen was referring to a June 2021 run on Iron Finance’s Titan token, which fell in value from $65 to $30 in two hours. Iron Finance later said the run was due to a few big holders selling off their shares, causing others to panic.

Earlier this month, US President Joe Biden issued an executive order calling for more research into the development of a national digital currency through the Federal Reserve Bank, or “The Fed”. Lawmakers then followed with their own bill, calling on the Treasury to create an electronic dollar – a virtual representation of a US dollar.

The Thunes survey found that one of the most important factors for Zoomers when it comes to shopping and payment methods is brand trust; it was cited as the main factor in choosing a primary payment method in seven of the 13 countries surveyed, including western and emerging markets.

S&P Global Market Intelligence 451 Research

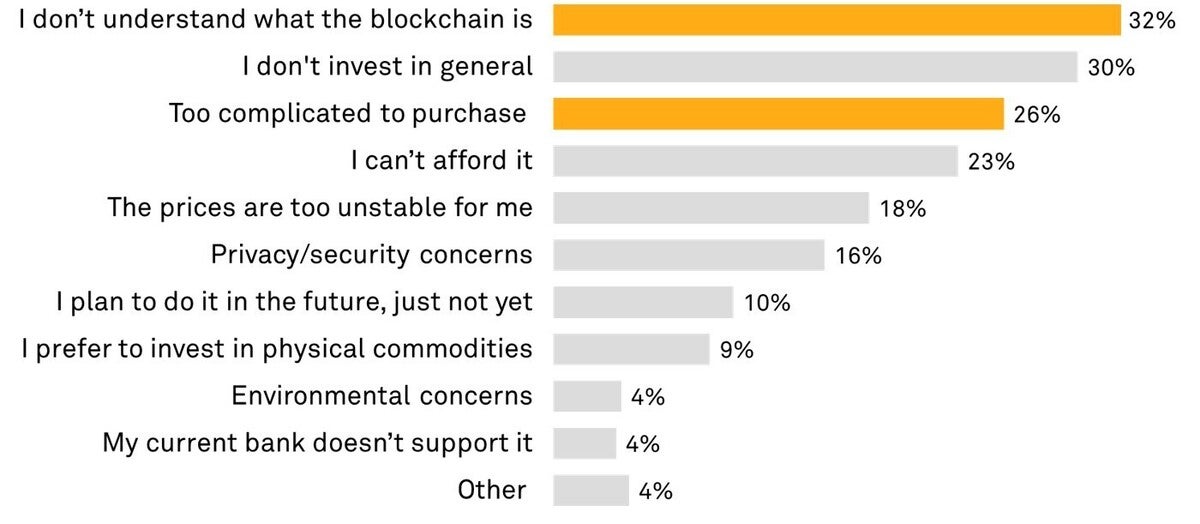

S&P Global Market Intelligence 451 ResearchWhy didn’t you participate in cryptocurrency trading?

User experience was identified as the second most popular factor, which in an online world also affects loyalty.

“For many, Gen Z is a misunderstood and overlooked generation,” Thunes CEO Peter De Caluwe said in a statement. “This is a generation for whom ‘dial-up’ and ‘desktop’ are meaningless words and who don’t just think ‘mobile-first’, but live and breathe in apps, social media, digital platforms and soon – the metaverse.We should start taking this generation seriously because the revenues and strategic plans of many companies – especially those that rely on rapid growth – depend on it.

The 451 Research report says that while financial institutions have largely avoided direct participation in cryptocurrency so far, its survey indicated several potentially lower-risk entry points, including:

- Redemption of rewards and loyalty points for cryptocurrency. This could help issuers increase their appeal to millennials, more than half of whom (52%) have expressed interest in this use. Startups such as Bakkt are already moving in this direction.

- Receive cryptocurrency instead of credit or debit card reward points. Square, through its Cash Card, is an example of an issuer that already allows cardholders to earn cryptocurrency for making certain purchases (for example, receiving 5% cash back in Bitcoin for a restaurant transaction). Interest in this option was clear among high-income cardholders — 45% of respondents with annual household incomes over $125,000 liked the idea.

- Link debit cards to cryptocurrency balances. Most cryptocurrency exchanges issue cards that consumers can deploy to draw down their cryptocurrency balances for in-store and online purchases, just like they would using a debit card linked to their checking account. . Card issuers could partner with exchanges to link cardholders’ cryptocurrency balances to their existing debit cards – 42% of Gen Z and 47% of Millennials expressed interest in the idea .

Gen group. Z/Zoomers has nearly 2.5 billion people worldwide; it surpassed millennials in terms of population in 2019.

Mobile wallets are gaining ground in emerging markets where bank accounts have historically been difficult to access and financial exclusion is widespread. Mobile phone providers have led a digital payments revolution in Asia, while in Africa, major telecom providers have offered similar digital payment solutions, the Thunes report notes.

Social media is part of Gen Z’s daily life and is increasingly driving their economic activity. More than nine in 10 Gen Zers say they now use social media throughout the day, and the number of platforms they connect to continues to grow. Seven out of 10 in the survey said they bought products discovered on social media, such as Facebook and Tik Tok. TikTok is quickly catching up with YouTube, Facebook and Instagram in popularity.

Thunes and 451 Research surveys shed light on how the world’s youngest, most digitally savvy consumers are forcing changes to decades-old business practices.

“Failure to recognize the looming influence of digital native Zoomer could lead to declining sales of a once perfectly shoppable brand,” Caluwe said.